Tuesday, August 31, 2010

Barristas, Potters, Yoga Instructors and Depression Economics

Brad de Long has a great introduction to Depression Economics here. Can't wait for lecture 3.

Wednesday, August 25, 2010

Real Estate as an Investment?

The lastest US new home sales numbers hit new record lows in July and am amazed how long this downcycle is. Inventory numbers are close to the lows of 40 years ago when population and household numbers were much lower but no sign of a rebound in sales.

Calculated risk has the analysis and the charts as usual:

The Baseline Scenario ponders why so many believe real estate is such a good investment after all. Looking at this long term chart nothing to be too excited about. Exclude bubble years and real real estate prices in the US have barely moved over longer time periods:

They argue:

"Housing is generally a worse investment than either stocks or simple U.S. Treasury bonds. Then why do so many people think it’s such a great investment?

Calculated risk has the analysis and the charts as usual:

The Baseline Scenario ponders why so many believe real estate is such a good investment after all. Looking at this long term chart nothing to be too excited about. Exclude bubble years and real real estate prices in the US have barely moved over longer time periods:

They argue:

"Housing is generally a worse investment than either stocks or simple U.S. Treasury bonds. Then why do so many people think it’s such a great investment?

- Leverage. Let’s say inflation is 2% and housing returns 3% (1% real return). If you put 10% down, now your house is returning 30%, or a 28% real return; subtract a 6% fixed-rate mortgage, and you’re making about 22%–or twenty-two times the real return of the underlying asset. Of course, we all know the dangers of leverage.

- Price illusion. People remember the nominal price they paid for their houses. When they sell them thirty years later, they look at the difference between the nominal purchase and sale prices and think they made a ton of money. This is especially true of the generation that bought houses in the 1960s and early 1970s before inflation hit; they saw their home prices go up by a factor of ten and thought it was due to high real returns.

- Bubbles and optimism bias. Every now and then we have a huge bubble like the one at the right-hand end of the chart above. For a while, people think that’s the new normal. For a while after that, they continue to think it’s the new normal, because they are biased toward optimistic expectations about the world. (Note that during the first half of the decade that I was advising friends that housing was a bad investment, housing was actually a great investment, assuming you could get out in time.)"

Monday, August 23, 2010

Druckenmiller Quits

One of the hedge fund great is retiring. Bloomberg has the story with some interesting infos on the man who broke the ERM.

From the article:

"He made some of his biggest trades working with Soros, including one that cemented Soros’s reputation as a preeminent speculator: A $10 billion bet in September 1992 that the Bank of England would be forced to devalue the pound.

From the article:

"He made some of his biggest trades working with Soros, including one that cemented Soros’s reputation as a preeminent speculator: A $10 billion bet in September 1992 that the Bank of England would be forced to devalue the pound.

Breaking the Bank

By August of that year, Druckenmiller said he had initiated a $1.5 billion trade that would profit if the German mark rose versus sterling. He expected Europe’s exchange-rate mechanism, in which the currencies moved against each other within a limited band, to come under pressure as Germany raised interest rates to prevent inflation after reunification. Germany’s move forced the United Kingdom and other members of the ERM to decide whether to increase rates, which could damage their already troubled economies, or devalue their currencies and fall out of the ERM.

Druckenmiller said he calculated that the Bank of England didn’t have enough reserves to prop up the currency, and it couldn’t afford to raise rates. He was right, and selling by the Soros fund is credited with pushing the pound out of the ERM.

“He was so proud because until that point Soros had never made $1 billion on a bet,” said Roger Entress, a Pittsburgh surgeon and early Duquesne investor, who was golfing with Druckenmiller at the National Golf Links of America in Southampton, New York, the weekend before the devaluation."

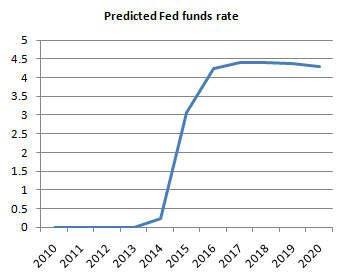

A Bond Bubble?

Prof Paul Krugman does not think so. Using a simplified Taylor Rule and projections for employment and inflation from the CBO he derives a predicted fed fund rate which looks like this:

Low rates for years to come!!!

He adds: "That’s right: four years of near-zero short-term interest rates. Does a 10-year rate of 2.6 percent still sound so unreasonable? And bear in mind that I’m not using some doomsayer’s forecast; I’m using the staid folks at the CBO.

Low rates for years to come!!!

He adds: "That’s right: four years of near-zero short-term interest rates. Does a 10-year rate of 2.6 percent still sound so unreasonable? And bear in mind that I’m not using some doomsayer’s forecast; I’m using the staid folks at the CBO.

And just for the heck of it, I asked what interest rate on a 10-year security would yield the same present value as investing in short-term debt at the predicted rates, and rolling it over each year. (Actually, I cheated slightly, because I was getting tired; I considered a bond in which there are no payments along the way, just repayment of accumulated interest and principal in year 10; but I’m pretty sure it doesn’t make much difference).

And the implied interest rate was … 2.6 percent.

Here’s what I think is going on: aside from the obviously intense desire of some of the bond bubble folks to see a fiscal crisis — they’ve been planning for it, and they’re not going to take no for an answer — my sense is that a lot of people just can’t bring themselves to face the reality that we’re likely to be in a zero-interest world for a long time. They just keep assuming that the Fed is going to raise rates soon, even though there is absolutely nothing about the macro situation that would justify such a rate increase."

If no bubble and the bond market is right expect some dismal economic prospects for much longer. Bu hao!

Market Update

Econbrowser has a great analysis of where we stand market valuation wise. Using Prof Shiller's data he posts the following charts:

(1) 17% downside to be back to average

(2) A chart comparing PE and the following 10 year nominal returns of the S&P500. At the current PE do not expect much in the next years if history is any guide

(3) And among others a chart comparing the dividend yields vs tips' and bond yields.

While equities do not strike as bargains they still compare favourably to bonds.

He concludes: "A buyer of stocks today is usually getting a higher immediate yield than on TIPS, in addition to prospects of future dividend growth. Just as they did in the 19th century, stocks as priced today should give you a significantly better return than bonds"

(1) 17% downside to be back to average

(2) A chart comparing PE and the following 10 year nominal returns of the S&P500. At the current PE do not expect much in the next years if history is any guide

(3) And among others a chart comparing the dividend yields vs tips' and bond yields.

While equities do not strike as bargains they still compare favourably to bonds.

He concludes: "A buyer of stocks today is usually getting a higher immediate yield than on TIPS, in addition to prospects of future dividend growth. Just as they did in the 19th century, stocks as priced today should give you a significantly better return than bonds"

Thursday, August 12, 2010

Dividend Aristocrats 2010

Here is the list of the 42 companies from the S&P500 that have raised their dividends for 25 years in a row or more. In the past they have outperformed the S&P500 substantially.

| 3M Co | MMM |

| AFLAC Inc | AFL |

| Abbott Laboratories | ABT |

| Air Products & Chemicals Inc | APD |

| Archer-Daniels-Midland Co | ADM |

| Automatic Data Processing | ADP |

| Bard, C.R. Inc | BCR |

| Becton, Dickinson & Co | BDX |

| Bemis Co Inc | BMS |

| Brown-Forman Corp B | BF/B |

| CenturyLink Inc | CTL |

| Chubb Corp | CB |

| Cincinnati Financial Corp | CINF |

| Cintas Corp | CTAS |

| Clorox Co | CLX |

| Coca-Cola Co | KO |

| Consolidated Edison Inc | ED |

| Dover Corp | DOV |

| Emerson Electric Co | EMR |

| Exxon Mobil Corp | XOM |

| Family Dollar Stores Inc | FDO |

| Grainger, W.W. Inc | GWW |

| Integrys Energy Group Inc | TEG |

| Johnson & Johnson | JNJ |

| Kimberly-Clark | KMB |

| Leggett & Platt | LEG |

| Lilly, Eli & Co | LLY |

| Lowe's Cos Inc | LOW |

| McDonald's Corp | MCD |

| McGraw-Hill Cos Inc | MHP |

| PPG Industries Inc | PPG |

| PepsiCo Inc | PEP |

| Pitney Bowes Inc | PBI |

| Procter & Gamble | PG |

| Sherwin-Williams Co | SHW |

| Sigma-Aldrich Corp | SIAL |

| Stanley Black & Decker | SWK |

| Supervalu Inc | SVU |

| Target Corp | TGT |

| VF Corp | VFC |

| Wal-Mart Stores | WMT |

| Walgreen Co | WAG |

Subscribe to:

Posts (Atom)